Tologs need to learn financial literacy

The Council for Economic Education

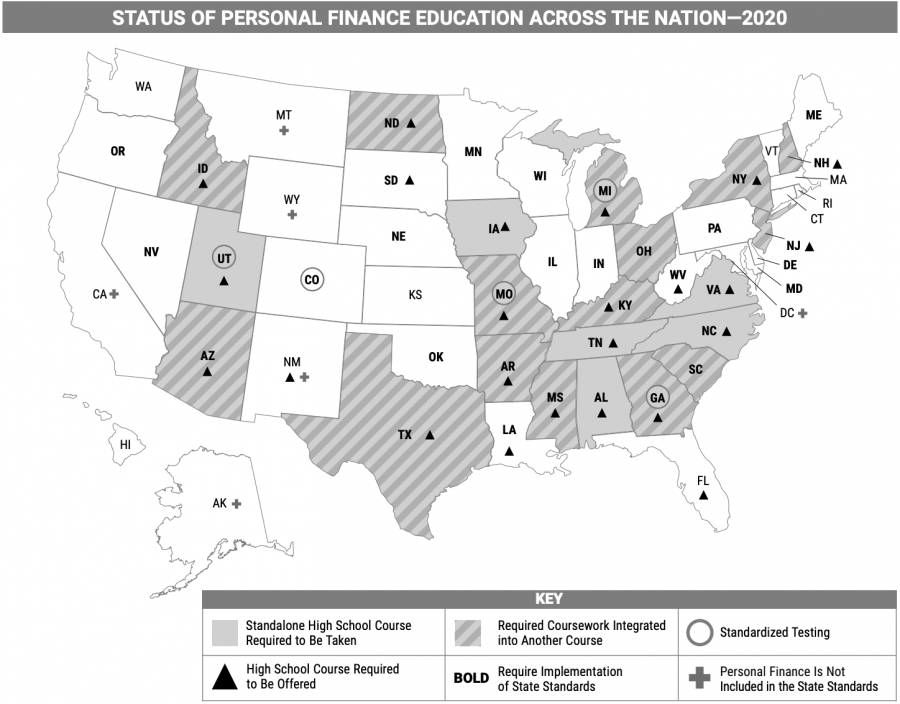

The Council for Economic Education surveyed all 50 states in 2020 on the extent of their high school financial literacy education requirements.

I have a wide smile on my face when I walk out on my first payday after work at Abercrombie Kids in Arcadia. It’s a summer day, and in my hand is my first real paycheck after a hard day on the job.

“I may be making minimum wage, but it’s better than nothing,” I think to myself.

But wait. I look at my check, and the math doesn’t add up. For my four hours of work, I should have more than what is written on the check. Where did the other money go?

I talk to my parents about my confusion, and they give me a reality check.

“Social Security and Medicare taxes come out of your paycheck. That’s where your money went. If you start to make enough money, you’re going to have to pay other taxes too,” my mom says.

My head is running a million miles a minute because now I’m caught up thinking about paying taxes. I know my parents file tax returns every year; am I going to have to do this too?

This question, among others, is a common one in my friend group as financial literacy — basic financial skills such as investing, managing money and budgeting — isn’t taught at Flintridge Sacred Heart or California public schools. There are five states in the U.S. that do not have a state standard for financial literacy education in school, one of them being California.

Based on a TIAA Institute study conducted in 2020 about financial literacy, only 53% of adults in the United States answered more than half of the financial questions correctly on a test.

Statistics like these make it all the more important to start teaching high schoolers about personal finances so they are prepared for the real world. According to a Google Consumer study from 2016, one in three Americans has $0 saved for retirement. If people could have learned the importance of saving at a younger age, this could have been prevented for some Americans. In the same Google Consumer survey, 51% of millennials said that their lack of personal finance knowledge is keeping them from making financial progress.

Another significant problem is student debt, which is totaled at about $1.52 trillion currently. With proper financial education, high school seniors can learn about debt and how that factors into college decisions.

Financial literacy is a topic that should be taught to all high school students in order to prevent rising adults from entering society without the help of their parents. Understanding one’s finances is crucial for survival in today’s world. According to a 2017 report from the George Mason University Mercatus Center, Utah — a state with required financial literacy education in high school — is one of the “top five most fiscally healthy states.” A 2018 study in U.S. News and World Report ranked Utah the number one state for fiscal stability. According to The Institute for College Access and Success, Utah also has the least amount of student loan debt compared to other states as of 2021.

I know that required financial literacy instruction is not the only reason that has made Utah successful in the above criteria, but I believe financial literacy instruction can only help.

While FSH does have an economics class that covers some of the basics, a more in-depth class is necessary for students to be able to thrive in life after high school.

“It’s good that you take the economics class to understand some of the broader levels of econ,” Assistant Principal for Curriculum and Instruction Mrs. Sherrie Singer said. “We’re hoping that you develop a sense of how you might make decisions about general economics through the econ class, but it doesn’t have the application you might experience in a financial literacy course.”

The current economics class, which is required for graduation, gives an overview of essential topics such as the stock market, credit cards and savings.

“With a lot of the families we support, these types of conversations [about financial literacy beyond what appears in the economics class] often happen organically in the homes,” Singer said.

While parents may bring this up at home, learning it in a classroom can only enrich education about finances.

In an ideal world, I envision a year-long course similar to Utah’s curriculum for high school students, which was the only state to receive an A+ grade from Champlain College’s Center for Financial Literacy for its financial literacy education.

Both California public schools and FSH should adopt their standards.

Here’s how I imagine a financial literacy class at FSH playing out.

The first part of the class would be focused on basic economic principles including opportunity cost and supply and demand in order to have general knowledge about economics before delving into more complex topics.

Next, students would learn about different types of jobs, the skills needed to perform those jobs and how income plays a role in this.

Students would then focus on investing and saving. This includes the stock market, how to buy and sell stocks and how to save for retirement and the various types of retirement plans.

The next part of the class would concentrate on budgeting, credit, debt and how the government plays a role in personal finances.

Finally, the last unit would be all about taxes and how to pay them. Many high school students have jobs, and they should understand where part of their paycheck goes. It is also crucial to know when people have to start paying federal, state and local taxes. Students will learn about filing tax returns themselves because even though many parents are kind enough to do it for their kids right now, they will soon find themselves alone and not knowing what to do.

Just as high schools teach students writing, chemistry and U.S. history, they have an obligation to prepare students for the reality of life after school. This includes teaching the basic financial skills needed to succeed in the world.

Jessie Mysza is the managing editor for the Vertias Shield. She started writing for the Shield her sophomore year and served as an associate editor her...